This article is sponsored by Bain & Company

Corporate carve-outs routinely produce some of the flashiest returns in private equity, right? Well, yes and no.

Before 2012, the typical carve-out deal generated an average multiple on invested capital (MOIC) of around 3.0x versus the 1.8x average for all buyout deals. Since then, top-quartile carve-outs have continued to produce great returns: a 2.5x MOIC versus the 2.7x top-quartile buyout average. But the average carve-out deal since 2012 has earned just a 1.5x MOIC, or slightly below the broader buyout average.

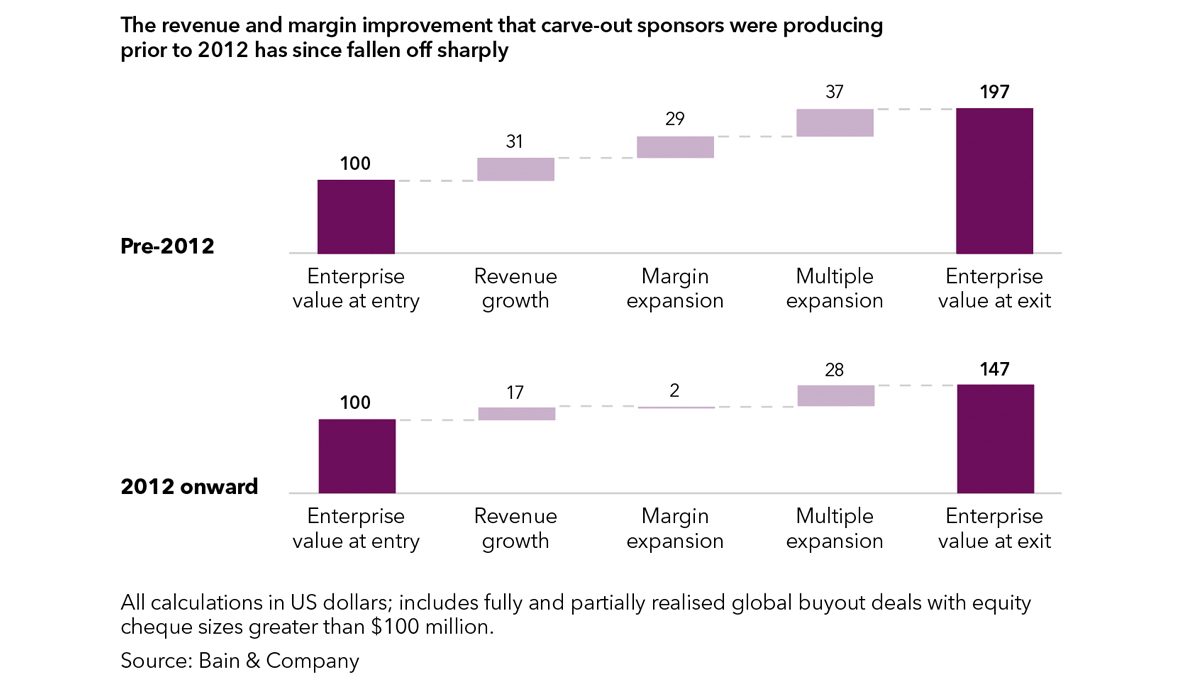

What’s changed is that sponsors aren’t delivering the operational improvements they once did. Carved-out companies increased enterprise value during ownership in the pre-2012 period by boosting revenue and margins 31 percent and 29 percent, respectively. Those numbers have slipped to 17 percent and 2 percent since 2012, and multiple expansion has fallen commensurately (see chart). Competition, meanwhile, has increased sharply, pushing up sale multiples and challenging sponsors to up their game.

Criteria for success

Looking at a sample of 25 carve-outs between 2013 and 2024, the common denominator for success is clear: winning sponsors ensure that there is an unbreakable link between the value creation thesis propelling the deal and how the new company is set up to achieve it.

While that might sound obvious, it’s a lot less common than you’d think. Given the complexity of separating a business from its parent, PE investors and their advisers too often “stand up” a newly independent company first and worry about fixing it second. This two-step process only adds complexity to complexity.

The most certain (and de-risked) path is to underwrite a bulletproof value creation plan in due diligence before using it to shape the separation plan, talent strategy and execution blueprint. Value creation, in other words, drives the agenda.

It’s true that extricating the business from its corporate parent adds an extra layer of difficulty to carve-outs. Seasoned sponsors quickly assess what’s included in the deal perimeter (as opposed to being held back by the parent) and the implications of that list. Planning must account for a spaghetti bowl of interdependencies with the parent across critical functions like finance, human resources and IT. Clean separation requires amending hundreds or thousands of agreements with third parties while drafting ironclad transition service agreements (TSAs), which lay out the services and support the seller will extend to the new company for a defined period of time.

As critical as all of that is, however, the difference between separating and separating well comes down to the value creation plan. The overarching deal rationale prioritises what’s essential to achieve and in what sequence.

Consider one global medical technology company that had struggled to grow profitably as part of a much larger conglomerate. The business offered a strong set of testing products for mid-market customers. But the parent’s emphasis on top-line growth led it to expand internationally into 97 countries.

Due diligence showed the company had no clear idea of how profitable each of those 97 markets was. So, instead of trying to stand up all of them in the separation plan, the new team analysed the performance of each and scaled them back to the 10 that were most profitable, creating new, indirect models for the rest. The company then hired 50 new salespeople and developed playbooks to refocus on the more promising US market. The new, built-for-purpose operating model turned things around, eventually producing an MOIC of 2.9x at exit.

Tough decisions can’t wait

One reason large, bureaucratic businesses often underperform is that leaders kick sensitive or painful decisions down the road – perpetually. Carve-outs need to make the right decisions for the business right away.

For example, that’s what Platinum Equity did when it acquired Emerson Electric’s Network Power business unit in 2016 and renamed it Vertiv. The business made equipment vital to the large data centres that were fast taking over cloud computing. But diligence showed that Emerson was focused on customers that were building one-off data centres, rather than the hyperscale cloud service providers and colocation providers emerging as leaders. Several potential bidders, in fact, backed away from the deal early, concluding it was already too late to make up lost ground with these new customers.

Platinum was willing to bet it could reshape the new company fast enough to compete in the larger arena. It cut costs and sold a noncore business to de-risk the investment and then set about zero-basing the operating model. It revamped product development, the go-to-market organisation, manufacturing operations, and functions like finance and HR. An aggressive new CEO got rid of silos that were slowing things down and created a customer-focused operation dubbed “One Vertiv” aimed squarely at the mega data centres. As the boom in artificial intelligence sent demand for these scale players into overdrive, Vertiv thrived. The result: a blockbuster IPO, giving Platinum a strong partial exit.

Matching leadership to mission

As is often the case, making that leadership change proved essential for Vertiv. Many carve-outs come with capable leaders who have grown up in a cosy, slow-moving corporate world. Yet PE-backed carve-outs are anything but cosy and slow-moving. Managers may underperform when asked to dial up the metabolism. Or they might lack the specific skills necessary for executing the new strategy.

Again, the value creation plan should be the guide here. It will define which roles and functions are needed, and when, to deliver on the deal’s ambition. That provides a fact base for installing the right people, whether they come from inside or outside the company.

What we’ve seen from the recent drop-off in carve-out performance is that it’s never been harder to pull off one of these uniquely challenging transactions. But with a clear deal thesis unifying the separation and value creation agendas, sponsors can move rapidly from day one to generate next-level performance.

Greg Schooley is a partner in Bain & Company’s PE practice and leads the operational value creation team. Ben Siegal is a partner in the M&A practice and leads Bain’s carve-out solution. Colleen von Eckartsberg is Americas leader of the M&A practice and a leader in the technology, customer strategy and marketing, and PE practices